The latest solitary-large MH must be situated in a rural region of your to stand a window of opportunity for qualifying to possess an excellent USDA-recognized financing. Predict lenders for different more conditions on the financial.

- Creditworthiness (you should have a good checklist out of repaying loans or expense)

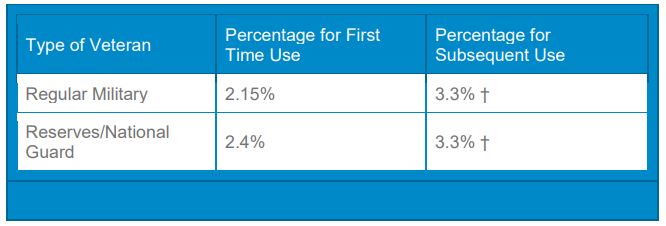

Carry out USDA Funds Want PMI?

USDA finance do not require personal mortgage insurance, the standard which have antique mortgages. Although not, they attract a few investment fees which can be fairly the same as PMI.

Anticipate paying an upfront be sure commission of just one % from your own home loan matter. Additionally shell out an annual percentage out of 0.thirty-five per cent of the overall loan amount.

USDA-accepted lenders usually roll-out the latest initial percentage throughout the financing number and assume one pay they throughout the closing.

They also fees brand new yearly fee once yearly and you may divide it towards the monthly installments that you ought to spend along with other monthly loan financial obligation.

In the event one another upfront and you may annual charges is actually billed whatever the down-payment you will be making, he is method less expensive than private mortgage insurance rates.

It is possible to imagine a traditional home loan to invest in the acquisition away from a single-wider MH since it comes with favorable mortgage conditions and you will rates of interest. This loan can be match your investment means for those who have an enthusiastic higher level credit rating and you may a reduced personal debt-to-income ratio.

Type of Traditional Loans to have MH

The average sorts of conventional finance become compliant antique funds, non-compliant antique money, fixed-rates antique financing, and you may variable-speed old-fashioned funds.

A compliant traditional loan is commonly below or equivalent to an enthusiastic FHFA (Government Houses Money Agency) -recognized financing limitation.

The fresh new FHFA kits this limit a-year to mirror maximum loan count Freddie Mac or Fannie mae can buy. Loan providers make use of credit history and financing installment capability to be considered you on the financing.

Non-compliant traditional money always go beyond the newest FHFA compliant restriction. They are used buying a home which have a top purchase price compared to the conforming restriction.

not, expect you’ll run into rigorous underwriting procedures based on bucks supplies, deposit, and you can credit rating required for cash advance in Hamilton Alabama acceptance from the lenders.

Fixed-price old-fashioned financing have a predetermined interest rate, when you find yourself adjustable-rates mortgages (ARMs) provides rates of interest one to change-over go out. Arm cost usually are in line with the economy rates of interest.

Being qualified to own a conventional Home loan

Good credit and you may deposit will be the finest requirements getting antique money if you’d like to get just one-large MH. Since the old-fashioned fund commonly secured otherwise covered by government bodies, predict more strict eligibility standards.

Individual mortgage brokers feel the versatility in order to demand stricter conditions than just direction passed by Freddie Mac computer, Fannie mae, and you will FHFA.

Ergo, some think it’s challenging to qualify whenever obtaining a mortgage shortly after case of bankruptcy otherwise foreclosures. The qualifications standards are the pursuing the:

Good credit Rating

A credit history of 740 or higher can be entitle that reduce costs and attractive interest rates. The lender make a difficult query to review the borrowing from the bank in advance of giving your with the loan.

Low Obligations-to-Earnings Proportion

Most personal mortgage lenders anticipate you to definitely have a financial obligation-to-earnings ratio (DTI) below thirty six percent when applying for a normal mortgage.

Their DTI reflects the quantity of money you will be due since the personal debt split up by the monthly earnings (ahead of income tax). Consider using a debt-to-income calculator so you’re able to imagine their DTI in advance of trying to an MH mortgage.

As much as 20% Advance payment

A decreased downpayment you can previously purchase a traditional MH financing is 3 %. Yet not, you pay far more when you have a leading debt-to-earnings ratio and lower credit score.